HIDING INCOME & ASSETS at the IRS

In family law, forensic accountants focus on valuing marital estates, determining which assets and liabilities may be non-marital, determin- ing the parties’ incomes, and calculating alimony and child support.

With clients (or their spouses) who receive a W-2, calculating net income should be easy. Many divorcing couples have at least one party who is employed, receives a regular paycheck, and has federal income taxes withheld from each paycheck. Within certain boundaries, the taxpayer determines the amount of tax withheld by filing a W-4 form with the employer.

Here is an example of how a W-2 employee tried to use the IRS to conceal marital assets for distribution, and to hide income for support.

Hiding Income

In 2014, my client (the wife), filed for divorce. The husband, who was pro se, was a marketing manager for a large corporation, and was, therefore, a W-2 employee. Through her attorney, the wife engaged me to value the marital estate and to determine her husband’s income.

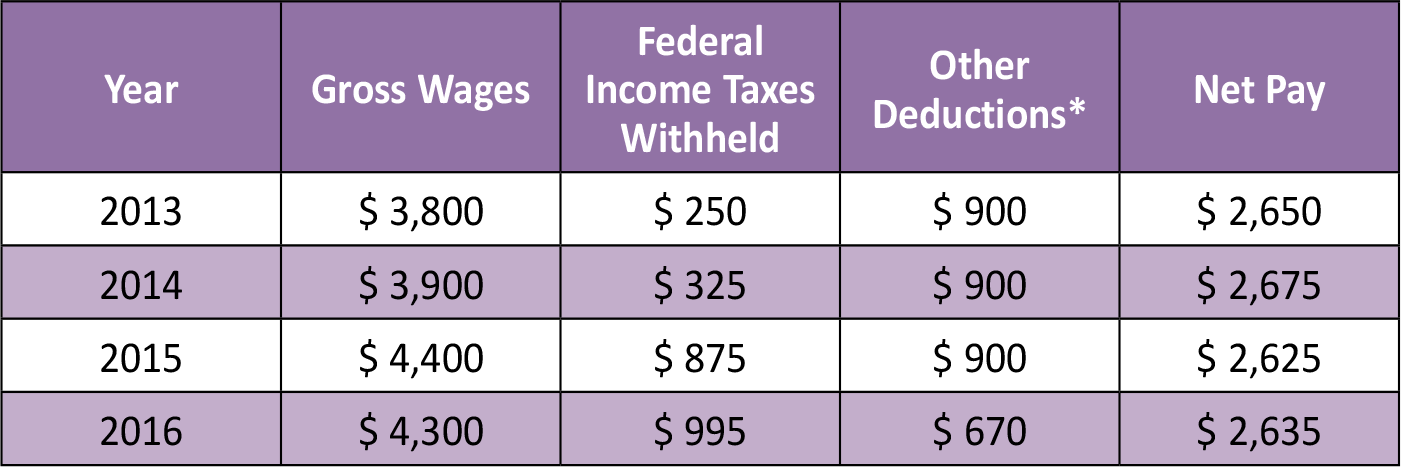

In 2014, the husband was ordered to pay the wife temporary support of $800 per week, or $1,600 bi-weekly. At the time, the husband’s bi-weekly gross income was $3,900 and his net income was $2,675. After paying temporary support, he was only left with $1,075 per pay period. The husband requested another hearing to reduce his temporary support obligation, which was reduced to $400 per week, or $800 bi-weekly.

The wife was not able to sustain at that level, so she requested another hear- ing, and the temporary support was adjusted to $600 weekly, or $1,200 on a bi-weekly basis. Under that scenario, the husband was able to retain $1,475 bi-weekly from his $2,675 net pay.

In 2015, the husband received a raise, bringing his bi-weekly gross wages from $3,900 to $4,400. His withholding have been around $350. After other deductions, his net pay shoul have been about $3,150. After tempo-rary support to his wife of $1,200, the husband should have netted $1,950 bi-weekly during the temporary support period.

However, the husband decided to increase his federal withholding taxes to $875 per pay period. This had the effect of reducing his bi-weekly net pay to $2,625, or approximately the same level as 2014, thereby hiding his $13,000 annual pay increase.

In December of 2015, the husband again wanted to reduce his temporary support obligation. He came to court with a pay stub that showed net pay of $1,875, and claimed that his pay was reduced. With temporary support payments of $1,200 to his wife, the husband claimed that he only had $675 per pay period, while his wife had $1,200.

Upon closer examination, there was a one-time adjustment of $750 (net of taxes) that caused the husband’s bi-weekly net pay to go from $2,625 to $1,875 that one pay period that he brought to court. Using the IRS as an accomplice, the husband was able to demonstrate, with his pay stubs, that his bi-weekly net income in 2014 was $2,675 and his bi-weekly net income in 2015 was $2,625, in spite of a 13% pay increase.

In 2014, the husband was ordered to pay the wife temporary support of $800 per week, or $1,600 bi-weekly. At the time, the husband’s bi-weekly gross income was $3,900 and his net income was $2,675. After paying temporary support, he was only left with $1,075 per pay period. The husband requested another hearing to reduce his temporary support obligation, which was reduced to $400 per week, or $800 bi-weekly.

The wife was not able to sustain at that level, so she requested another hear- ing, and the temporary support was adjusted to $600 weekly, or $1,200 on a bi-weekly basis. Under that scenario, the husband was able to retain $1,475 bi-weekly from his $2,675 net pay.

In 2015, the husband received a raise, bringing his bi-weekly gross wages from $3,900 to $4,400. His withholding have been around $350. After other deductions, his net pay shoul have been about $3,150. After tempo-rary support to his wife of $1,200, the husband should have netted $1,950 bi-weekly during the temporary support period.

However, the husband decided to increase his federal withholding taxes to $875 per pay period. This had the effect of reducing his bi-weekly net pay to $2,625, or approximately the same level as 2014, thereby hiding his $13,000 annual pay increase.

In December of 2015, the husband again wanted to reduce his temporary support obligation. He came to court with a pay stub that showed net pay of $1,875, and claimed that his pay was reduced. With temporary support payments of $1,200 to his wife, the husband claimed that he only had $675 per pay period, while his wife had $1,200.

Upon closer examination, there was a one-time adjustment of $750 (net of taxes) that caused the husband’s bi-weekly net pay to go from $2,625 to $1,875 that one pay period that he brought to court. Using the IRS as an accomplice, the husband was able to demonstrate, with his pay stubs, that his bi-weekly net income in 2014 was $2,675 and his bi-weekly net income in 2015 was $2,625, in spite of a 13% pay increase.

Summary of Husband’s bi-weekly wages, taxes, deductions, and net pay

*Other deductions include social security taxes, Medicare taxes, and health insurance

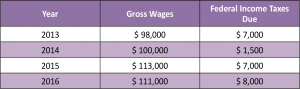

Summary of Husband’s annual wages and taxes

Hiding Assests

In addition to hiding income, this husband also managed to hide assets at the IRS.

From 2013 to 2016, the husband’s gross wages showed modest annual increases. During the same time period, the husband’s income taxes were never more than $8,200.

In 2014, the year that the wife filed for divorce, the Husband sent a $20,000 estimated tax payment to the IRS. This unnecessary payment, plus some ordi- nary excess withholding, resulted in an overpayment of about $27,000 in 2014. The husband received a refund of $3,000, leaving $24,000 to apply to the following year’s (2015) taxes.

In 2015, the husband increased his withholding, adding about $16,000 in overpayments to the IRS. After filing his 2015 tax return, the husband had almost $40,000 in refunds available at the IRS, but not requested.

In 2016, the husband again over-withheld his (W-2) federal income taxes, adding an additional $17,000, to his IRS “savings account.” The funds secreted in the US Treasury totaled over $57,000 at the end of 2016 – and some portion of those funds were marital.

From 2013 to 2016, the husband’s gross wages showed modest annual increases. During the same time period, the husband’s income taxes were never more than $8,200.

In 2014, the year that the wife filed for divorce, the Husband sent a $20,000 estimated tax payment to the IRS. This unnecessary payment, plus some ordi- nary excess withholding, resulted in an overpayment of about $27,000 in 2014. The husband received a refund of $3,000, leaving $24,000 to apply to the following year’s (2015) taxes.

In 2015, the husband increased his withholding, adding about $16,000 in overpayments to the IRS. After filing his 2015 tax return, the husband had almost $40,000 in refunds available at the IRS, but not requested.

In 2016, the husband again over-withheld his (W-2) federal income taxes, adding an additional $17,000, to his IRS “savings account.” The funds secreted in the US Treasury totaled over $57,000 at the end of 2016 – and some portion of those funds were marital.

Pitfalls for the Abuser

It would seem logical that the IRS should be happy when taxpayers overpay or withhold excess taxes. However, the tax code prohibits such behavior. The code identifies certain practices as frivolous, and applies penalties for filing frivolous tax returns. The Internal Revenue Code section 6702(a) lists positions (taken when filing a tax return) that constitute frivolous filing. Included in paragraph (22):

“…an amount of withheld income tax or other tax that is obviously falsebecause it exceeds the taxpayer’s income as reported on the return or is disproportionately high in compari- son with the income reported on the return…” The penalty for filing a frivolous tax return is $5,000. Of course, it is safe to say that most judges do not look kindly on litigants who engage in such dishonest practices.

“…an amount of withheld income tax or other tax that is obviously falsebecause it exceeds the taxpayer’s income as reported on the return or is disproportionately high in compari- son with the income reported on the return…” The penalty for filing a frivolous tax return is $5,000. Of course, it is safe to say that most judges do not look kindly on litigants who engage in such dishonest practices.

Conclusion

Just because your client is a W-2 employee does not mean that you don’t need a forensic accountant on your team.

With an MBA from MIT and a Masters in Accounting, Harriett Fox (CPA) specializes in com- plex financial analyses in divorce proceedings. She has served as an expert witness in numerous cases, and she is a Collaborative Financial Professional. www.harriettfoxcpa.com

Related Article

How Do You Find Hidden Assets?

Suggestions for how to go about locating hidden assets: questions to ask, places to look and things to look for.

www.familylawyermagazine.com/

articles/find-hidden-assets

As a Certified Public Accountant with many years of experience, Harriett Fox provides attorneys, divorcing couples and businesses with forensic accounting services. As a collaborative financial professional, Harriett works with divorce attorneys and helps couples to settle out of court.

As a Certified Public Accountant with many years of experience, Harriett Fox provides attorneys, divorcing couples and businesses with forensic accounting services. As a collaborative financial professional, Harriett works with divorce attorneys and helps couples to settle out of court.

Harriett was born and raised in Newton MA, a suburb of Boston. She holds an MBA from the Sloan School of Management at MIT, and a Master of Accounting from FIU. She has worked in positions at Fortune 500 companies, family owned businesses, and international, national and local accounting firms. She was recently appointed to the Florida Bar Grievance Committee – Eleventh Judicial Circuit.

Harriett has had her own forensic accounting practice in Coconut Grove for over 10 years. She is devoted to minimizing the damage caused by divorce by helping families navigate and communicate using the collaborative divorce process

![]()

![]()

harriettfox@alum.mit.edu

T: 305.495.2179

www.harriettfoxcpa.com

Facebook | Linkedin | Youtube